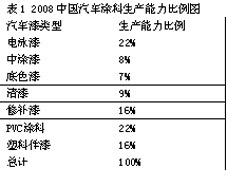

Automotive coatings include automotive body paints, automotive refinishes, auto parts paints, and PVC anti-knock paints. The original car paint is the paint used for the uniform painting of the car before leaving the factory. The general definition refers to the car body paint that can enter the car's paint line and can be baked in the workshop. The body paints of cars, minivans, medium vans and minivans are mostly automotive paints. Automotive refinish is literally referring to lacquer used for car surface repair care. However, in China, the body paints of most large passenger cars and trucks are refinish paints, and they account for a very large part of refinish paint. Automotive parts paint refers to the paint used in bumper paint, automotive interiors, fittings, etc., such as front and rear bumpers, fenders, wheel covers, doors, instrument panels, protective panels, water tank masks, etc. Bumper paint accounts for the vast majority of parts paint. PVC anti-stone strike coating is mainly used for automobile chassis and fenders. The main base material is PVC resin. China Automotive Coatings Market Overview Since the second half of 2008, due to the impact of the global financial turmoil and the National III standard, the production and sales of passenger cars and commercial vehicles, and the growth rate of exports both fell. Among them, the growth rate of passenger vehicles slowed down by 60.28% in the second half of the year, and the growth of commercial vehicles was 39.37% slowed. However, after entering the year of 2009, due to the introduction of policies such as the reduction of purchase tax by half for 1.6 liters of the auto industry adjustment and revitalization plan on January 14, 2009, and the introduction of policies for the automobile to the countryside, the demand for the Chinese passenger car market rebounded in the first quarter, and the sales volume was about Up to 2 million vehicles, an increase of 7.8% year-on-year, of which sales of cars have exceeded 1.4 million, an increase of 3%. However, the commercial vehicle market is still sluggish. In the first quarter of 2009, the sales volume of commercial vehicle main products was only 680,000 units, which was a year-on-year decline of more than 30%. Nevertheless, China’s overall automobile sales exceeded the United States in the first quarter, which was the world’s largest. In 2008, China’s nearly 200,000 tons of automotive paint production capacity was mainly concentrated in three regions: East China, Central South, and North China. The northeast, southwest and northwest are relatively small, but with the continuous increase of labor costs and raw material costs in the eastern coastal areas, the southwestern region, which is dominated by the municipality of Chongqing, has become an important growth point for future profit of some OEMs. In 2008, the demand for new car coatings in China was about 205,000 tons, auto repair paint was 70,000 tons, parts paint was 30,000 tons, and PVC paint was about 70,000 tons. The proportion of various types of paint production is roughly as shown in Table 1. China Automotive Coatings Market Share In the Chinese original paint market, 75% to 80% of the market share was occupied by international brands; in the refinish market, about 75% of the market share was occupied by domestic brands, but most of them occupied low-repair paints. End market; In the plastic paint market, most of the market share is still an international brand. With regard to the amount of bicycle coatings, due to the improvement of the performance of automotive coatings and the continuous improvement of coating technology, the performance that can only be achieved if a thick film is required before can now be satisfied in the state of a film, and the amount of single paint for automobiles gradually decreases, and a new car is currently used. The amount of paint used was only 60% 10 years ago. At present, the main automotive paint manufacturers are: Kansai (Hunan, Tianjin, Chongqing, Shenyang), BASF, DuPont, PPG, Nippon, KCC; major refinish paint manufacturers are: Guangzhou Shichuang, Guangzhou Bonny, Changzhou Plena, PPG, Guangzhou United, Changzhou Fullem, Guangzhou Foton, Guangzhou Arto, DuPont, AkzoNobel, Sherwin, Valspar, BASF, Nippon, KCC, etc. Analysis of Key Manufacturers in Chinese Automobile Industry ◆ Kansai Kansai’s automotive coating layout in China was intended to correspond to the location of China’s major automakers in order to be able to supply coating products locally, such that Kansai’s automotive coatings have won in Northeast China, Beijing, Tianjin, Hubei, Guangdong and Chongqing. Major market share of major production plants. Among them, Hunan Kansai Automotive Coatings Co., Ltd. was established in February 1995 with Japan's Kansai Paint Co., Ltd. It is the most complete automotive OEM supplier in China, and it is FAW, Second Automobile, Shanghai Volkswagen and SAIC. General Motors, Guangzhou Honda, Changan Automobile, Chongqing Ford and Southeast Automotive, and other domestic 27 major automotive manufacturers provide services, including automotive primer, middle coating, and 55 topcoat coating lines. ◆PPG In China, major customers of PPG automotive coatings include Volkswagen, GM, Mercedes-Benz, BMW, Dongfeng Peugeot, Citroen, Chery and Hainan Mazda. Almost all car manufacturers around the world use PPG's automotive coating products or technologies. In 2002, Chery invested 700 million yuan to purchase the most advanced coating production line from Germany. Afterwards, PPG invested 70 million yuan in the first phase to build a factory and specialized in the production of paints for Chery in Wuhu. Starting in June 2008, it can meet the demand for high-quality paint for 1 million cars per year, which not only cements Chery’s existing advantages in the automotive paint field, but also provides Chery’s capacity to expand production capacity. In addition, PPG is accelerating internal integration and plans to build a new automobile paint factory in Guangzhou outside of the Wuhu project and gradually improve its layout in the domestic automotive paint industry. ◆Nippon In 2005, Libang began to introduce waterborne automotive paints to China's major automotive production lines, and established with China's Guangzhou Honda, Tianjin Xiali, Tianjin Toyota, Wuhan Honda, China Honda, Xiangfan Nissan, Hainan Mazda, Jinbei Automobile and Changan Suzuki. Cooperation relationship. Among them, Nippon Paint is mainly for Japanese cars, domestic cars, Great Wall, Shuanghuan and BYD and other vehicles also have some Nippon share. Nippon provides pre-processing, electrophoresis, middle coating, topcoat, and bumper coating products including traditional solvent-based intermediate and topcoats, and makes them domestically produced. Nippon also subordinated to Rohm & Haas Company in 2006 in the United States. The automotive coating business is being integrated into the bag, combining the automotive body coating business with the plastic coating business to achieve a global development strategy. Nippon's automotive paint production was distributed in Shanghai, Guangzhou and Langfang before 2008. The thinner part of the automotive paint has been transferred to Chengdu, and the rest of the automotive paint production will be officially transferred to Chengdu by 2009 at the latest, and will also serve the automotive paint business in Chengdu, Chongqing, Wuhan, Xi’an, and Guizhou. Unlike Kansai’s automotive coatings layout in China, the establishment of Nippon (Chengdu) allowed Nippon Paint to provide a full range of coating products and services in East China, South China, Southwest China, and North China. Competition for the market share of automotive paint adds weight. [next] DuPont By gradually increasing its stake in DuPont Hongshi Coatings (Beijing) Co., Ltd. from 51% to 76% and also acquiring a 100% stake in DuPont Hongshi Paint (Changchun) Co., Ltd., DuPont China has increased China Automotive Investment in the Coatings Industry. DuPont provides all-round services such as electrophoresis, middle coating and topcoat for the public, Chengdu Toyota, Chongqing Ford, Jianghuai, Harbin Hafei, Wuhan Citroen, Baoding Great Wall and Changchun Hongqi. In addition, a new paint production facility for DuPont Performance Coatings was recently put into production in Jiading District, Shanghai, China. The construction plan of the new plant was made in the second quarter of 2006. The new plant will be mainly used to produce automotive refinish products to meet the needs of the automotive refinish market in China. In addition to refinish products, it will also provide coatings designed for trucks, heavy equipment and many industrial applications in the rapidly growing Asia-Pacific region. DuPont joined Changchun Taioua Paint Co., Ltd. and became a controlling shareholder. DuPont's goal is to make the company the largest and most advanced automobile paint production base in China. ◆ BASF BASF Shanghai Coatings Co., Ltd. is BASF's only company producing automotive coatings in China. Most of BASF’s business comes from European and American cars, including DaimlerChrysler, Shanghai Volkswagen, Shenyang BMW Brilliance, and Yantai General Motors, among which Shanghai Volkswagen has the largest market share; in addition, BASF and Nissan In the cooperation relationship of the automobile in Japan, BASF Shanghai Paint Co., Ltd. shared part of the business from Nissan Nissan, and also occupied a significant share of the business volume of BASF Shanghai Paint Co., Ltd. ◆ Akzo Nobel AkzoNobel Automotive Refinish is a division of the AkzoNobel Group. Its paint products are mainly for surface refinishing or repainting of automotive bodies. Customers include repair stations, distributors, large-scale enterprise fleets, automotive suppliers and major Manufacturers of cars and trucks, including Sikkens, Lesonal and Miluz. Aksu Nobel launched a new service system at the Beijing FAW Toyota 4S store a few days ago. AkzoNobel's Sikkens automotive refinishment passed the quality test of General Motors Europe (GM) in 2007, and new brand auto refinish was tested to meet the common series Chevrolet and Daewoo. Repair requirements for Daewoo, Vauxhall and Saab brand cars. This means that GM's auto repair center will use the Shingen brand of automotive refinish paint for car repair work in the near future. China Automotive Coatings Price The domestic automobile original paint market is a relatively closed market. Original paints are sold directly from the original paint supplier to the car manufacturer through direct sales, resulting in the sales of each paint of each original paint to different car manufacturers. The price is different. The price of the same brand-specified automotive paint sold to domestic cars and imported cars may differ by 50%. In the domestic automotive OEM paint market, price vicious competition has occurred in recent years. Even if they are all foreign brands, in order to compete for market share, the average price (including CED, Zhongtu, and topcoat) will also be from 25 yuan/kg to 35 yuan. Wide fluctuations between / kg. In several automotive paint coatings, the price of electrophoretic paint is the lowest, but the profit of electrophoretic paint is the highest. The price of topcoats, depending on the color, can be quite different. Because automotive paint itself has relatively high requirements, most of auto paint raw materials are purchased from foreign countries; because multinational companies have global procurement systems, they have advantages in terms of price and transportation costs. Refinish paint is the most profitable part of current automotive paints. PPG, DuPont, and Nippon set up technical service and R&D departments for refinish paint in China respectively, but core technologies and mass production are almost completed overseas. Since most of the refinish lacquer is sold in the 4S shop, the refinish lacquer's primary sale price and secondary sale price are different. The average sales price of foreign brand refinish paint is around 70-85 yuan/kg. The difference in color will lead to the difference in price. Plain (black and white) is relatively cheap, but red and yellow are relatively high in price, and the price of pearlescent glitter is the highest. Domestic auto refinish has its own advantages, its quality is close to imported products, the price is only imported 1/2 ~ 2/3; In addition, domestic auto refinish paint developed according to the needs of the domestic auto market, more and more in the Chinese auto refinish market Dominant. However, the domestic auto refinish market is very chaotic. At present, there are hundreds of brands, most of which are private enterprises, and individual plants hit the market with inferior products. In general, the demand for automotive paint is increasing, and the price of automotive paint has not increased. This situation has already reduced the profits of auto paint to less than 10% or even negative profits. Whether to compete for market share and lower prices or maintain prices to maintain profits has become a problem many auto paint manufacturers have to face in the next few years. Development Outlook Maergehua predicts that the growth rate of China's automobile sales will be around 5% in 2009, passenger cars will be slightly higher than commercial vehicles, which will increase by 6% to 7%, while the small-displacement passenger car market will pick up while heavy. In the field of special vehicle coatings for trucks, agricultural vehicles, etc., Maergeland is expected to grow to a certain extent. In February 2009, Shandong Province ranked first in China for the first time because of its dense industrial cluster of special vehicles, with a total output value of 19.2 billion yuan in the automotive industry surpassing that of production in Guangdong Province. It is estimated that by 2012, China’s auto production will reach 12 million vehicles, requiring a total of 480,000 tons of automotive coatings, including about 250,000 tons of new vehicle paint, about 95,000 tons of refinish paint, and parts and paint and PVC stone-resistant paint. Up to 135,000 tons or so, for the automotive coatings production companies under the financial crisis is still a certain amount of room for growth.

Table 1 2008 proportion of China's auto paint production capacity